Why San Jose?

It’s a question I’m asked a lot by investors in the course of their due diligence. What makes Urban Catalyst think that, of all the cities around the country, San Jose has a strong demand for office?

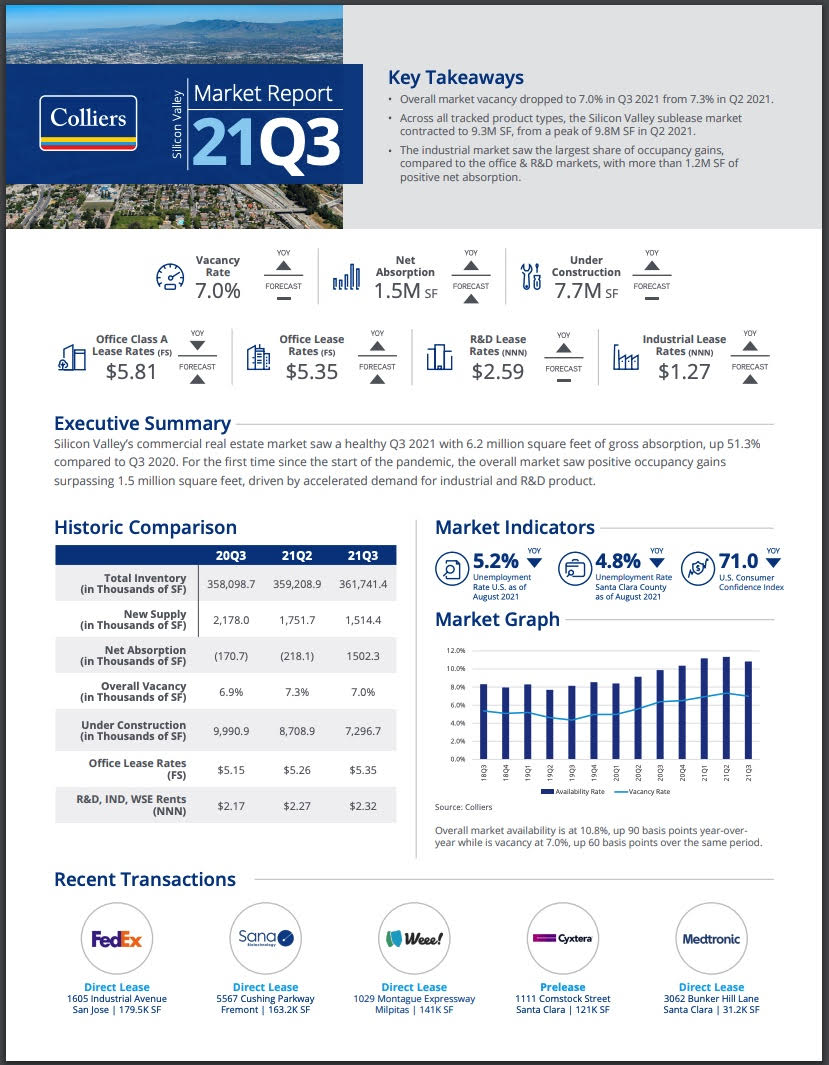

The answer: We listen to the experts—experts like Colliers, a global commercial real estate firm.

A preview of Colliers’ third-quarter 2021 report on the region finds Silicon Valley’s office market is making a strong comeback from the economic obstacles created by the coronavirus, the Mercury News’ George Avalos reported.

The average monthly rental price of $5.35 a square foot is “the highest on record” in Silicon Valley, Lena Tutko, Colliers research director, said.

Colliers considers the Silicon Valley office market to be composed of Santa Clara County and Fremont.

Colliers report regarding commercial real estate in Silicon Valley in Q3

Sean Toomey, a Colliers senior vice president, said: “Silicon Valley is absolutely emerging from the doldrums of the pandemic and stay-at-home mandates. This is further noted by increases in traffic on our Silicon Valley freeways, ridership on Caltrain, and in tenant touring as many companies prepare for a projected January return-to-work environment.”

Other positive signs noted in the Mercury News article are:

- An increase in rent in a variety of commercial types of space—office, research and industrial space.

- There’s been a decrease in vacancies for industrial and research space.

- There’ve been more than 2 million square feet of office leasing transactions for two consecutive quarters.

Why San Jose? Ask the experts at Colliers; they’ll tell you.>

Remember that the potential 10% reduction of capital gains taxes disappears on Jan. 1, 2022.

Important Disclosures

The contents of this communication: (i) do not constitute an offer of securities or a solicitation of an offer to buy securities, (ii) offers can be made only by the confidential Private Placement Memorandum (the “PPM”) which is available upon request, (iii) do not and cannot replace the PPM and is qualified in its entirety by the PPM, and (iv) may not be relied upon in making an investment decision related to any investment offering by an issuer, or any affiliate, or partner thereof ("Issuer").

All potential investors must read the PPM and no person may invest without acknowledging receipt and complete review of the PPM.

With respect to any performance levels outlined herein, these do not constitute a promise of performance, nor is there any assurance that the investment objectives of any program will be attained. All investments carry the risk of loss of some or all of the principal invested. Assumptions are more fully outlined in the Offering Documents/ PPM for the respective offering. Consult the PPM for investment conditions, risk factors, minimum requirements, fees and expenses and other pertinent information with respect to any investment.

These investment opportunities have not been registered under the Securities Act of 1933 and are being offered pursuant to an exemption therefrom and from applicable state securities laws. All offerings are intended only for accredited investors unless otherwise specified.

Past performance are no guarantee of future results. All information is subject to change. You should always consult a tax professional prior to investing. Investment offerings and investment decisions may only be made on the basis of a confidential private placement memorandum issued by Issuer, or one of its partner/issuers. Issuer does not warrant the accuracy or completeness of the information contained herein. Thank you for your cooperation.

Real Estate Risk Disclosure:

- There is no guarantee that any strategy will be successful or achieve investment objectives including, among other things, profits, distributions, tax benefits, exit strategy, etc.;

- Potential for property value loss – All real estate investments have the potential to lose value during the life of the investments;

- Change of tax status – The income stream and depreciation schedule for any investment property may affect the property owner’s income bracket and/or tax status. An unfavorable tax ruling may cancel deferral of capital gains and result in immediate tax liabilities;

- Potential for foreclosure – All financed real estate investments have potential for foreclosure;

- Illiquidity – These assets are commonly offered through private placement offerings and are illiquid securities. There is no secondary market for these investments.

- Reduction or Elimination of Monthly Cash Flow Distributions – Like any investment in real estate, if a property unexpectedly loses tenants or sustains substantial damage, there is potential for suspension of cash flow distributions;

- Impact of fees/expenses – Costs associated with the transaction may impact investors’ returns and may outweigh the tax benefits

- Stated tax benefits – Any stated tax benefits are not guaranteed and are subject to changes in the tax code. Speak to your tax professional prior to investing.

Opportunity Zone Disclosures

- Investing in opportunity zones is speculative. Opportunity zones are newly formed entities with no operating history. There is no assurance of investment return, property appreciation, or profits. The ability to resell the fund’s underlying investment properties or businesses is not guaranteed. Investing in opportunity zone funds may involve a higher level of risk than investing in other established real estate offerings.

- Long-term investment. Opportunity zone funds have illiquid underlying investments that may not be easy to sell and the return of capital and realization of gains, if any, from an investment will generally occur only upon the partial or complete disposition or refinancing of such investments.

- Limited secondary market for redemption. Although secondary markets may provide a liquidity option in limited circumstances, the amount you will receive typically is discounted to current valuations.

- Difficult valuation assessment. The portfolio holdings in opportunity zone funds may be difficult to value because financial markets or exchanges do not usually quote or trade the holdings. As such, market prices for most of a fund’s holdings will not be readily available.

- Capital call default consequences. Meeting capital calls to provide managers with the pledged capital is a contractual obligation of each investor. Failure to meet this requirement in a timely manner could elicit significant adverse consequences, including, without limitation, the forfeiture of your interest in the fund.

- Opportunity zone funds may use leverage in connection with certain investments or participate in investments with highly leveraged capital structures. Leverage involves a high degree of financial risk and may increase the exposure of such investments to factors such as rising interest rates, downturns in the economy or deterioration in the condition of the assets underlying such investments.

- Unregistered investment. As with other unregistered investments, the regulatory protections of the Investment Company Act of 1940 are not available with unregistered securities.

- It is possible, due to tax, regulatory, or investment decisions, that a fund, or its investors, are unable realize any tax benefits. You should evaluate the merits of the underlying investment and not solely invest in an opportunity zone fund for any potential tax advantage.

The above material cannot be altered, revised, and/or modified without the express written consent of Urban Catalyst.