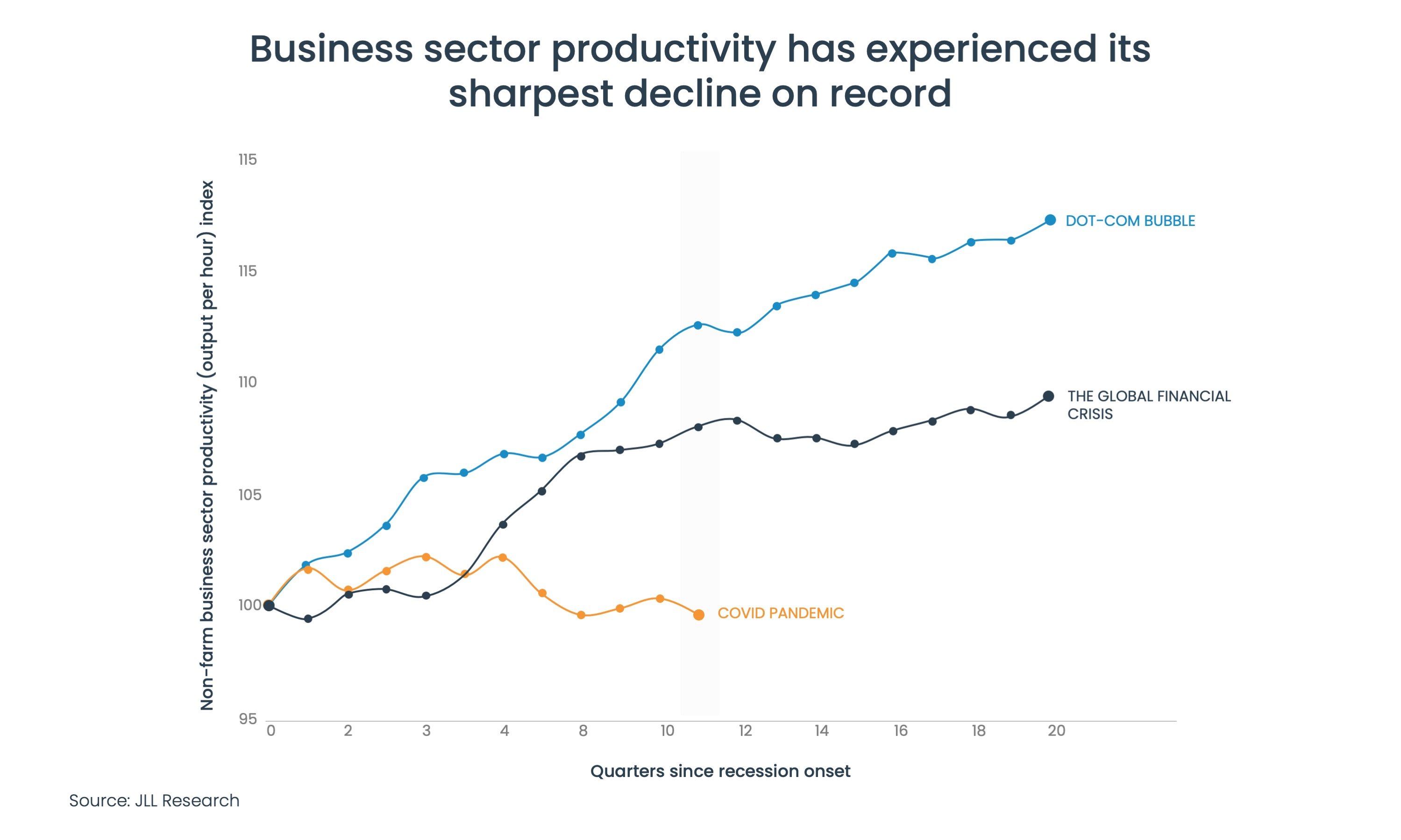

Since 2021, U.S. business sector productivity has experienced its sharpest decline on record, according to the Bureau of Labor Statistics. Now that the results are in and employers have that data, we’re seeing them make changes to increase productivity, including bringing employees back to the office. Many businesses have concluded that returning to in-office work is needed to increase efficiency and grow their bottom lines. Although these changes won’t bring every employee back to the office overnight, they will probably accelerate the return-to-office trend that’s been occurring since the end of the pandemic.

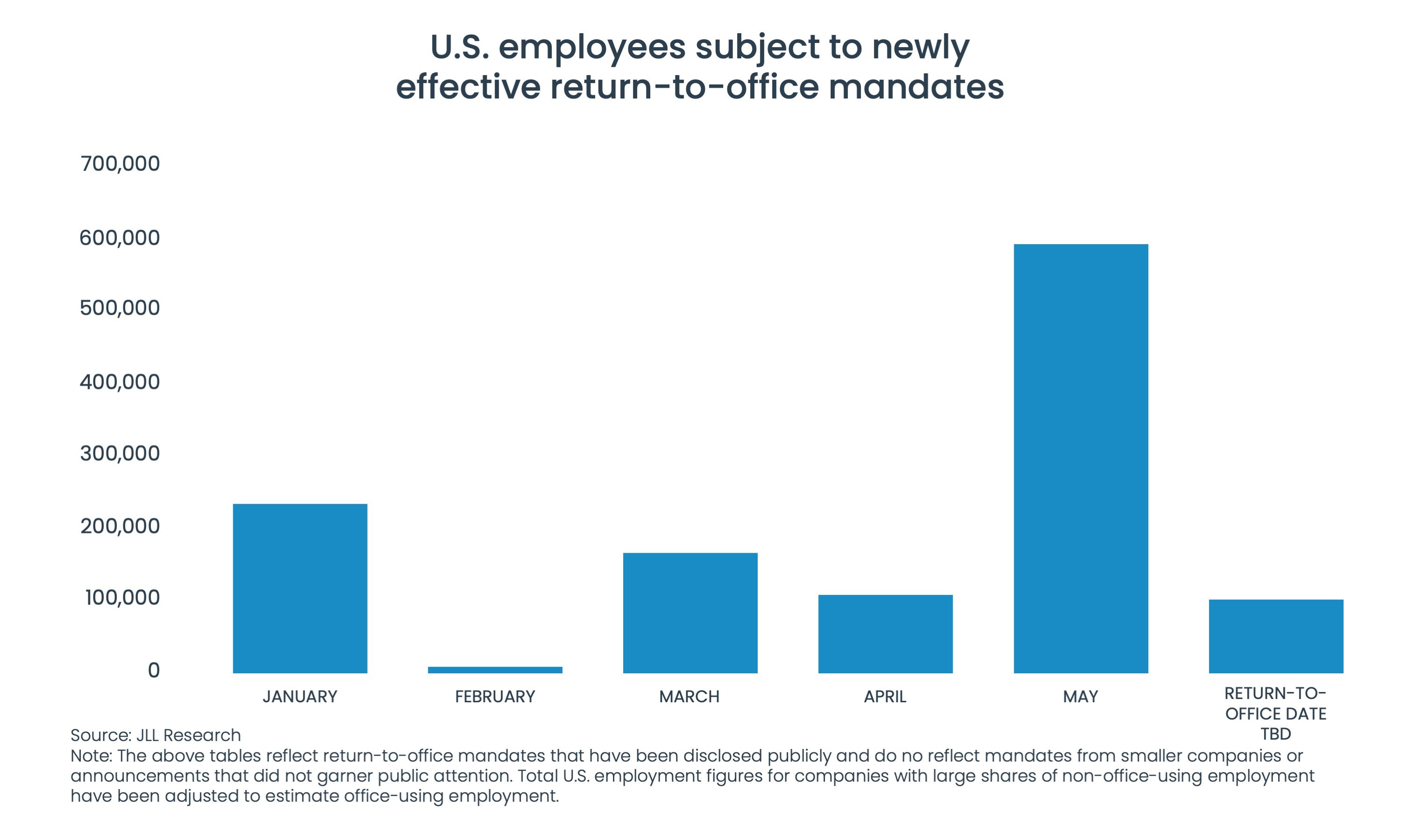

Companies aren’t delaying their return-to-office plans. Businesses nationwide rolled out stricter office mandates affecting over 500,000 employees in the first two weeks of May, according to JLL, a commercial real estate brokerage. That’s 22 percent higher than the number of employees impacted by office mandates between January and April, JLL reported last month. Although we can see the return-to-office trend in action, it will take some time — perhaps a couple of years — to return to what we would call the “new normal.”

Google’s email to employees last week outlining the tech company's plan to double down on office attendance is perhaps the most consequential example of how the tech sector has changed its tune on remote-friendly work policies. Google, whose 36,000-person workforce in Silicon Valley exceeds the populations of Menlo Park and Los Gatos, is widely considered a trendsetter in the tech industry and local economy. When Google changes its work policies, don’t be surprised if smaller and mid-sized companies across Silicon Valley do the same. From my experience, when Google talks, other companies listen.

Google also said it would start incorporating employees’ adherence to the company’s three-days-in-the-office-mandate into performance reviews, showing how much the company associates productivity with being in the office.

“Of course, not everyone believes in ‘magical hallway conversations,’ but there’s no question that working together in the same room makes a positive difference,” Google’s chief people officer Fiona Cicconi wrote in an email to employees last week, as reported by CNBC. “For those who are remote and who live near a Google office, we hope you’ll consider switching to a hybrid work schedule. Our offices are where you’ll be most connected to Google’s community.”

Google is only the latest large U.S. employer to partially or fully reverse remote-friendly work policies enacted early in the pandemic. Apple, which last year required all employees to work from the office three days a week, is tracking employee attendance through badge records and will give them “escalating” warnings if they don’t abide by that mandate, Business Insider reported in March. Amazon required its employees to return to at least three days of in-office work on May 1 after experimenting with fully remote, various hybrid, and full-time office models.

Amazon CEO Andy Jassy told employees in February that these models showed it's easier to “learn, model, practice, and strengthen our culture when we're in the office together most of the time and surrounded by our colleagues." Blackrock, the world’s largest asset manager, said it would increase in-office attendance requirements later this year to four days from three.

Not everyone has taken the stricter office mandates in stride; the Alphabet Workers Union — representing a relatively small, unidentified number of employees for Google’s parent, according to the Wall Street Journal — claimed that Google employees haven’t let their performance slip while taking advantage of flexible work arrangements.

However, those who’ve reviewed the latest U.S. worker productivity data may not buy the union’s assertion. The U.S. has had five consecutive quarters of year-over-year declines in productivity, according to an analysis of federal Bureau of Labor Statistics data by consulting firm EY-Parthenon.

Although the total amount of hours worked by U.S. employees increased by three percent from the fourth quarter of 2022 to the end of March, output grew just 0.2 percent. People are working longer hours and barely putting out more products, and you can’t cite time spent commuting to and from work as a reason since many employees are on hybrid or remote-first work schedules. I speculate that when people work from home, they’re not always working because if they were, the country’s productivity levels would be higher. Instead, they watch their kids, do their laundry, and maybe even binge-watch Netflix.

Businesses have spent much of the past three years searching for the right balance between pushing hard on office requirements and not alienating employees, who have generally had the upper hand in negotiating flexible work arrangements. Yet America is a capitalist society where productivity matters. And when the data says that business sector productivity nationwide has experienced its sharpest two-year drop ever, it’s clear whether a company’s survival will hinge on doing everything it can to increase productivity — including bringing its workers back to the office.

Are you interested in learning more about Urban Catalyst? Contact us today.

Important Disclosures

The contents of this communication: (i) do not constitute an offer of securities or a solicitation of an offer to buy securities, (ii) offers can be made only by the confidential Private Placement Memorandum (the “PPM”) which is available upon request, (iii) do not and cannot replace the PPM and is qualified in its entirety by the PPM, and (iv) may not be relied upon in making an investment decision related to any investment offering by an issuer, or any affiliate, or partner thereof ("Issuer").

All potential investors must read the PPM and no person may invest without acknowledging receipt and complete review of the PPM.

With respect to any performance levels outlined herein, these do not constitute a promise of performance, nor is there any assurance that the investment objectives of any program will be attained. All investments carry the risk of loss of some or all of the principal invested. Assumptions are more fully outlined in the Offering Documents/ PPM for the respective offering. Consult the PPM for investment conditions, risk factors, minimum requirements, fees and expenses and other pertinent information with respect to any investment.

These investment opportunities have not been registered under the Securities Act of 1933 and are being offered pursuant to an exemption therefrom and from applicable state securities laws. All offerings are intended only for accredited investors unless otherwise specified.

Past performance are no guarantee of future results. All information is subject to change. You should always consult a tax professional prior to investing. Investment offerings and investment decisions may only be made on the basis of a confidential private placement memorandum issued by Issuer, or one of its partner/issuers. Issuer does not warrant the accuracy or completeness of the information contained herein. Thank you for your cooperation.

Real Estate Risk Disclosure:

- There is no guarantee that any strategy will be successful or achieve investment objectives including, among other things, profits, distributions, tax benefits, exit strategy, etc.;

- Potential for property value loss – All real estate investments have the potential to lose value during the life of the investments;

- Change of tax status – The income stream and depreciation schedule for any investment property may affect the property owner’s income bracket and/or tax status. An unfavorable tax ruling may cancel deferral of capital gains and result in immediate tax liabilities;

- Potential for foreclosure – All financed real estate investments have potential for foreclosure;

- Illiquidity – These assets are commonly offered through private placement offerings and are illiquid securities. There is no secondary market for these investments.

- Reduction or Elimination of Monthly Cash Flow Distributions – Like any investment in real estate, if a property unexpectedly loses tenants or sustains substantial damage, there is potential for suspension of cash flow distributions;

- Impact of fees/expenses – Costs associated with the transaction may impact investors’ returns and may outweigh the tax benefits

- Stated tax benefits – Any stated tax benefits are not guaranteed and are subject to changes in the tax code. Speak to your tax professional prior to investing.

Opportunity Zone Disclosures

- Investing in opportunity zones is speculative. Opportunity zones are newly formed entities with no operating history. There is no assurance of investment return, property appreciation, or profits. The ability to resell the fund’s underlying investment properties or businesses is not guaranteed. Investing in opportunity zone funds may involve a higher level of risk than investing in other established real estate offerings.

- Long-term investment. Opportunity zone funds have illiquid underlying investments that may not be easy to sell and the return of capital and realization of gains, if any, from an investment will generally occur only upon the partial or complete disposition or refinancing of such investments.

- Limited secondary market for redemption. Although secondary markets may provide a liquidity option in limited circumstances, the amount you will receive typically is discounted to current valuations.

- Difficult valuation assessment. The portfolio holdings in opportunity zone funds may be difficult to value because financial markets or exchanges do not usually quote or trade the holdings. As such, market prices for most of a fund’s holdings will not be readily available.

- Capital call default consequences. Meeting capital calls to provide managers with the pledged capital is a contractual obligation of each investor. Failure to meet this requirement in a timely manner could elicit significant adverse consequences, including, without limitation, the forfeiture of your interest in the fund.

- Opportunity zone funds may use leverage in connection with certain investments or participate in investments with highly leveraged capital structures. Leverage involves a high degree of financial risk and may increase the exposure of such investments to factors such as rising interest rates, downturns in the economy or deterioration in the condition of the assets underlying such investments.

- Unregistered investment. As with other unregistered investments, the regulatory protections of the Investment Company Act of 1940 are not available with unregistered securities.

- It is possible, due to tax, regulatory, or investment decisions, that a fund, or its investors, are unable realize any tax benefits. You should evaluate the merits of the underlying investment and not solely invest in an opportunity zone fund for any potential tax advantage.

The above material cannot be altered, revised, and/or modified without the express written consent of Urban Catalyst.